Seventeen years ago, my spouse and I bought long-term care insurance. We were just about AARP-qualified at the time, and we were trying to get ahead of the age-related increases outlined above. The earlier you buy a plan, the cheaper it is. (Spouse is five years younger than I, so his rate was substantially lower than mine.)

The premiums have remained constant ever since. Until now.

Sticker shock!

My carrier is seeking to raise my rate by 338.6%. Three hundred and thirty-eight point six percent! Kind of defeats the purpose of buying early, doesn’t it? If our carrier can jack rates through the roof when we get older, the only thing we accomplished by buying early is donating tens of thousands of dollars to the company’s shareholders.

The proposed increase is awaiting approval by the Vermont Department of Financial Regulation. I spoke to a very nice lady in the insurance division of DFR, who told me it’s one of the biggest rate hikes she has ever seen — on any kind of insurance.

Last week, my spouse got a rate hike notice.

Of a non-whopping 20%.

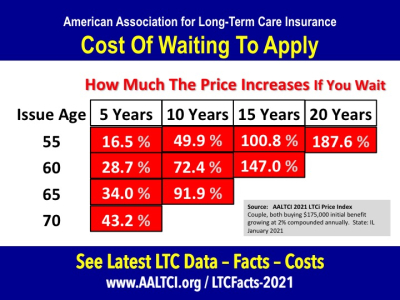

The only difference between us, as far as I can see, is that I’m 67 and my spouse is 62.

Looks a lot like age discrimination to me. Or like a carrier winnowing out its high-risk clients through targeted rate hikes.

This is the first time I’ve ever used this blog to write about an issue of personal concern. I’m doing this because I see a policy issue worthy of broader attention. How many clients does my carrier have in Vermont? Is it pulling the same stunt nationwide? Are other long-term insurers doing the same thing?

And what does it say about the cost/benefit of buying long-term insurance when your carrier can pull the rug out from under you at any time?

We could shop for an alternate carrier, but given the age/cost table above, that seems like an exercise in futility. Any quotes I get are likely to be unaffordable as well.

I’m filing a comment with DFR, for all the good that’ll do. If I’m lucky, they’ll knock a decimal place or two off the request and stick me with a tolerable increase. In which case I expect the carrier to try, and try, and try again until they either get the extortionate increase they want, or they nickel-and-dime me out of my policy.

I’ve done a little reading on the subject. The entire industry is claiming that it’s losing momey because people are living longer and are making more claims than they used to. Most carriers have left the business entirely, and there are roughly a dozen companies still in the business. Rate hike requests are endemic, although mine is definitely an outlier.

I can accept that payouts are on the rise. But these guys are supposed to be the experts at risk management. The entire industry is based on carriers getting to invest premium dollars until they have to make a payout, earning enough to be comfortably profitable while remaining able and willing to pay a claim when the time comes.

So the question is, how did the Brainiacs get this so wrong? And how did they manage to sail along blithely until things got so bad that they had to seek a gigantic rate increase all at once?

We bought these policies because the “system” for elder care in this country sucks rocks. Quality is iffy at best, and costs are so high that only the affluent can afford reliable care.

The backstop is Medicaid, which has two problems. First, in order to qualify, you have to spend down your assets to virtually nothing*. Second, the list of Medicaid-approved facilities is limited, and many of them are low quality.

*My sister and i faced this conundrum with our mother, who had modest assets to her name. We found a wonderful place for her, which did not accept Medicaid. We decided to admit her anyway and pay out of her estate. We were gambling that she would die before her money ran out. That’s a great feeling, let me tell you. “Fortunately,” she died which she still had some funds left.

Our inheritance was cut by about two-thirds. We didn’t really need the money, and were happy to spend it on security for Mom. But the system is a remarkably effective way to prevent working Americans from providing for their children after they die. It’s the ultimate in regressive taxation.

The whole system is full of bad choices and few, if any, good ones. Unless, again, you have enough wealth to buy your way into a positive situation. As long as we keep getting older and frailer in the aggregate, the problem will get worse. And I see no sign of the political will necessary to enact a solution.

Not in my lifetime, anyway.

Insurance, all kinds is a scam. You file a claim your premiums increase. I guess it is like death and taxes.

John, We have both retired now and are on Medicare, BS and BC supplimental and Medicare Part “D” with United Health supplimental perscription plan. Unless you are making a lot more than I think you are (Medicare is income sensitive) you shouldn’t be getting crushed by this ?

Long term care insurance is a separate thing from health insurance. It’s specifically meant to pay out if you have to enter assisted living.