The two House committees in charge of the state’s purse strings got together for a joint meeting Wednesday afternoon, and heard a solid hour of sobering news. The state has a substantial budget gap that seems to be widening by the day, and there is little appetite for the scale of cutbacks or tax increases necessary to close it. The two panels: Ways and Means, which acts on taxation and revenue; and Appropriations, which makes the spending decisions. In a tough budget year like this one, each of the two panels wanted to gain a better understanding of the challenges facing the other.

The bulk of the session was a walkthrough of proposed expenditures and revenues for the coming fiscal year, led by Joint Fiscal Office budget guru* Sara Teachout.

*Not necessarily her actual title.

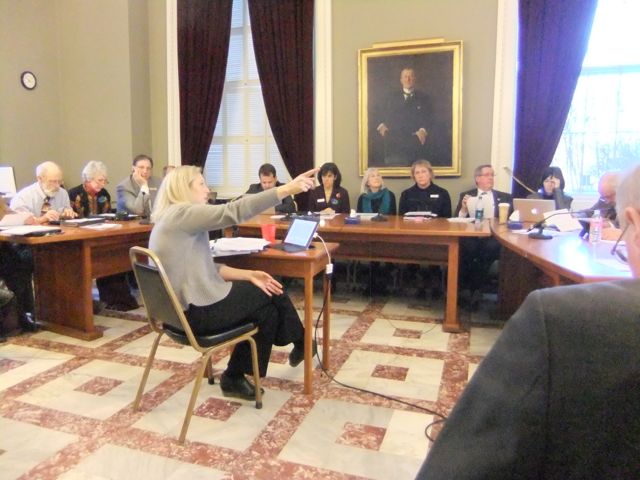

Sara Teachout of the Joint Fiscal Office, pointing to a large flatscreen display full of dispiriting numbers.

She began the session by outlining one of the little-known worms in the budgetary apple: cuts in spending would take effect on July 1, the start of FY 2016, but many of the potential revenue enhancements would not. For example: If the state eliminates a tax deduction on personal income, that revenue would not be realized until April 2016, when 2015 tax returns are due. That’s three-quarters of the way through FY 2016.

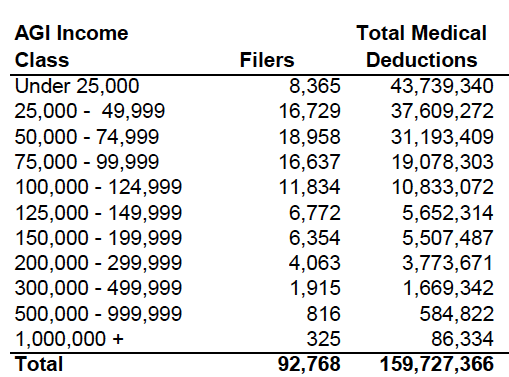

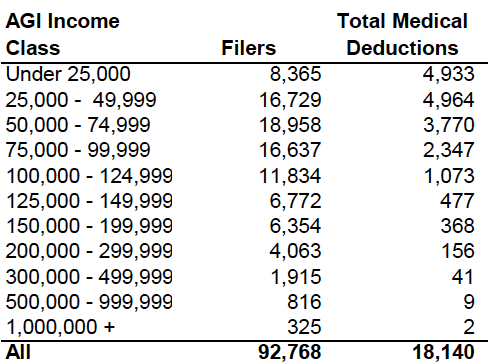

Much of Teachout’s presentation was a repeat of her tax-budget tutorial I heard at a recent Ways and Means meeting; I wrote three reports on the meeting, which can be found here, here, and here. (If you don’t want to wade through all three, do the last one first.) She did offer more detail at this joint meeting, including a very specific listing of the real costs of various tax expenditures and deductions. (All of her documents are posted on the Ways and Means webpage.)

There was some limited discussion after Teachout’s teach-in. Most significantly, Ways and Means chair Janet Ancel restated her support for a cap on tax deductions: “Speaking for myself, it’s the right thing to do if we’re looking for new revenue.” Rep. Mary Hooper, a member of the Appropriations Committee, noted that a cap on deductions “spreads out the impact, rather than zeroing in on specific exemptions or deductions.”

As I reported previously, Vermont’s tax rules allow the average million-dollar earner to claim hundreds of thousands of dollars in deductions. That’s why top earners pay an effective income tax rate of 5.1% instead of the statutory rate of 8.95%.

Two years ago, the House approved a cap on itemized tax deductions at 2.5 times the standard deduction; the measure died, mostly because of Governor Shumlin’s opposition. This year, he has signaled his openness to changing deductions and expenditures, even as he remains steadfast in opposing increases on his Big Three taxes: income, sales, and rooms & meals.

The cap would, IMO, greatly enhance the fairness of our state tax system. Currently, top earners pay a lower proportion of their earnings in state and local taxes than people in any other income group.

There was also some support in the room for looking at some of the sales-tax exemptions. For example, the state could impose a ceiling on clothing purchases — making them tax-exempt only below a certain dollar amount.

Rep. Mitzi Johnson, Appropriations chair, said her committee will “begin a conversaiton soon to lay out targets [for spending cuts].” She noted the importance of the joint meeting for gaining a clearer picture of “where the revenue could be coming from.”

The meeting was one more small step in what promises to be a long, grinding process leading to decisions that will make at least some constituencies unhappy. As one Statehouse observer told me — only half jokingly — “it might take until July” before they can work everything out.